It seems as though the list of risks to investors is rising. Supply chain imbalances, higher raw material costs, rising interest rates, labor shortages, and geopolitical risks each contribute to business risk – and therefore to market risk.

Investors are prudent to consider how these risks will play out in their portfolios. However, we believe it is important to stay invested even amid these risks. Cash can be a significant drag on a portfolio, especially when inflation is rising.

Instead, investors can employ expert asset allocation – choosing the asset classes that tend to outperform in a given macroeconomic environment – and, within each asset class, work with agile and skilled portfolio managers who can navigate the many changes we see.

Taking this approach, private credit is one of our highest conviction ideas for this macroeconomic environment. Where rising macroeconomic risk, such as higher inflation and interest rates, may negatively impact the yield of some credit asset classes, private credit is a floating-rate asset class, meaning the loan’s coupon rate resets or “floats” with the prevailing level of interest. As a result, the asset class has virtually no duration risk, making it well suited for a rising rate environment.

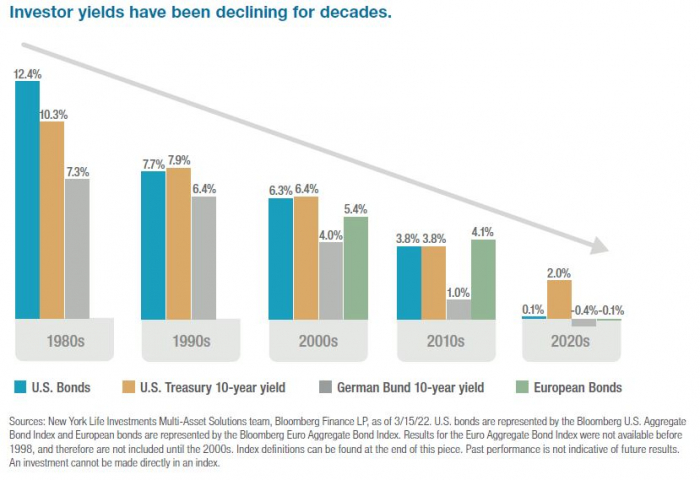

In addition, while interest rates are rising globally, many countries are experiencing negative real yields on government debt. Therefore, the absolute level of government bond yields is likely to remain anemic. Private credit provides investors with the opportunity for higher risk-adjusted return potential and a diversification of credit exposure.

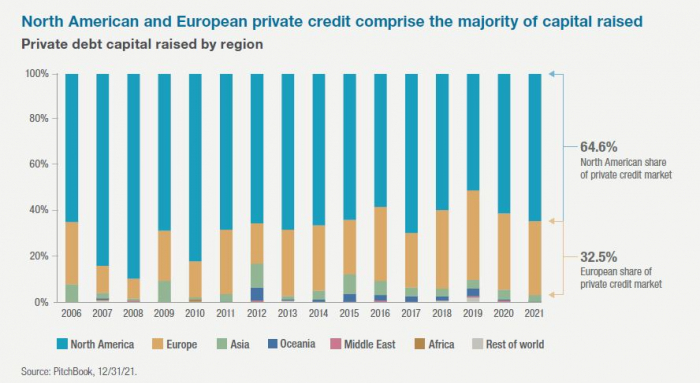

We invest in both U.S. and European private credit in our portfolios, and believe that doing so may allow investors to leverage the regions differing historical backdrops and funding environments. The U.S. is a large, mature, and fairly homogenous structure, while the European market is more fragmented. Documentation, origination strategy, competition, and banking structure vary by country. Together, these markets may offer opportunities for private credit partners who can navigate the respective challenges and opportunities of their regions.

Korean investors are sometimes less familiar with the European market for private credit, and so I focus my comments on a few important components of success there.

To begin, we are interested in the lower middle market of European private credit. The lower middle market is a segment which is underserved by the broader market and therefore benefits from reduced competitive pressures offering the deepest pool of opportunities in terms of number of companies. Targeting the lower middle market offers a significant number of advantages, such as larger deal selectivity and strong risk-adjusted returns amidst lower competition. Despite the opportunity, investors, and particularly those outside the U.S. and Europe, sometimes express concern that the lower middle market segment of private credit is riskier. For experienced investors, though, this simply need not be the case. For example, the lower middle market includes a large universe of diversified companies, allowing our investors to select a priority subset of names that can outperform the segment’s average risk and return. In addition, the lower middle market is strongly relationship-focused, which gives skilled investors the opportunity to use their expertise to potentially increase return. Deep connections and the ability to manage highly complex deals can result in reward for investors.

To leverage the lower middle market, we believe that considering sponsor-less deals and secondary markets are important aspects of opportunity. Investors accustomed to working with sponsor-driven deals or in primary-only markets may be concerned about the risks of these transactions. Here, too, context and manager skill are important. Just as one example, in Europe, sponsor-less deals make up the large majority – nearly 90% – of the universe of lending opportunities available. In other words, by focusing on the sponsor-less market, it could be said that investors expand their investment universe by around nine times. In our view, this allows our investment teams to avoid compromising on quality of management teams, information provided, collateral secured, and other essential investment items. In addition, negotiating with sponsor-less companies often provides a structural advantage, potentially allowing for better terms or bespoke opportunities.

In summary, we are highly confident in the European private credit opportunity, but as you can see, it is an asset class that requires an exceptional investment partner and where manager selection plays a central role. Skilled credit evaluation is key to assessing the best companies and limiting risks. Diversification of borrowers across industries helps build portfolio resiliency. Strong partnerships, backed by a long track-record in the market, provide access to the best deals and transparency into borrowers’ business operations. In our view, this increased transparency provides meaningful value in managing risk.

This is why we at New York Life Investments have entered a strategic partnership with Kartesia in December 2020. Kartesia is an €4 billion AUM, pan-European platform for private debt investment strategies, and builds on the strength that we have built in our U.S. private debt and private equity strategies to date. The team has a strong reputation in identifying mispriced and under-the-radar opportunities, with a focus on the lower-middle-market in Europe.

We believe strong managers with a proven track record of navigating economic cycles can generate a very interesting opportunity for investors. In our view, the breadth opportunities in the lower-middle market, a global approach, and understanding the right type of investment structure are essential to manager selection. Kartesia’s pan-European management team only strengthens our high-conviction view in this opportunity.

By Jae Yoon

Jae Yoon is the CIO of New York Life Investment Management, and Chairman of NYL Investments Asia. With over $650 billion in assets under management December 31, 2021, New York Life Investments is the asset management arm of New York Life Insurance Co. Kartesia is an affiliate of New York Life Investment Management.

We use cookies to provide the best user experience. By continuing to browse this website, you will be considered to accept cookies. Please review our Privacy Policy to learn our cookie policy.

Korean InvestorsKorean LPs name their 36 favorite alternative asset managers

Korean InvestorsKorean LPs name their 36 favorite alternative asset managers Korean investorsKorean LPs pick their 44 favorite alternative managers

Korean investorsKorean LPs pick their 44 favorite alternative managers![[Discussion] Think twice before heavy inflation hedge: NYLIM](/data/ked/image/2021/12/17/ked202112170012.145x94.0.png) New York Life Investments[Discussion] Think twice before heavy inflation hedge: NYLIM

New York Life Investments[Discussion] Think twice before heavy inflation hedge: NYLIM Artificial intelligenceMadison Capital Funding raises $460 mn from Korea

Artificial intelligenceMadison Capital Funding raises $460 mn from Korea Korea Post awards $436 mn real estate debt mandates to three US firms

Korea Post awards $436 mn real estate debt mandates to three US firms