For a piece of information to be desirable, it has to satisfy two criteria: it has to be important, and it has to be knowable. – Warren Buffett

Regular readers of my memos know that Oaktree and I approach macro forecasts with a high degree of skepticism. In fact, one of the six tenets of Oaktree’s investment philosophy states flatly that we don’t base our investment decisions on macro forecasts. Oaktree doesn’t employ any economists, and we rarely invite them to our offices to share their views.

The reason for this is simple: to use Buffett’s terminology, we’re convinced the macro future isn’t knowable. Or, rather, macro forecasting is another area where – as with investing in general – it’s easy to be as right as the consensus, but very hard to be more right. Consensus forecasts provide no advantage; it’s only from being more right than others – from having a knowledge advantage – that investors can expect to dependably earn above average returns.

Many investors think their job requires them to develop a macro outlook and invest according to its dictates. Successful stock pickers or real estate buyers often make pronouncements regarding the macro outlook, even in the absence of evidence linking their investment success to accurate macro forecasts. Nonetheless, since macro developments are so influential, many people think it’s downright irresponsible to ignore them when investing. Yet:

Most macro forecasts are likely to turn out to be either (a) unhelpful consensus expectations or (b) non-consensus forecasts that are rarely right.

I can count on one hand the investors I know who successfully base their decisions on macro forecasts. The rest invest from the bottom up, one investment at a time. They buy when they think they’ve found bargains and sell things they consider overpriced – mostly without reference to the macro outlook.

It may be hard to admit – to yourself or to others – that you don’t know what the macro future holds, but in areas entailing great uncertainty, agnosticism is probably wiser than self-delusion.

But why take my word for it? How about these authoritative views?

It’s frightening to think that you might not know something, but more frightening to think that, by and large, the world is run by people who have faith that they know exactly what’s going on. – Amos Tversky

It ain’t what you don’t know that gets you into trouble. It’s what you know for sure that just ain’t so. – Mark Twain

That brings me to the subject of forecasters’ track records, or rather the lack thereof. Back in the 1970s, an elder told me, “an economist is a portfolio manager who never marks to market,” and that description still seems highly appropriate. Have you ever heard an economist or macro strategist say, “I think there’ll be a recession soon (and xx% of my recession predictions have turned out to be right within a year)”? Would anyone invest with an investment manager who didn’t publish a track record? Why follow macro forecasters who don’t disclose theirs?

Finally, I want to point out that the same comments apply to most investors. You rarely hear them say they have no idea what the macro future holds or beg off from expressing opinions. One of the most important requirements for success in investing is self-assessment. What are your strengths and weaknesses? If you invest on the basis of your macro views, how often have they helped? Is it something you should keep doing or discontinue?

Having gotten everything off my chest concerning the shortcomings of forecasts, I’m going to devote the rest of this memo to thinking about the future. Why? To invert the Buffett quote that began this memo, the macro future may not be knowable, but it certainly is important. When I think back to the years leading up to 2000, I picture a market that largely responded to events surrounding individual companies and stocks. Since the Tech Bubble burst in 2000, however, the market has appeared to think mostly about the economy, the Federal Reserve and Treasury, and world events. That’s been even more true since the Global Financial Crisis in 2008. That’s why I’m devoting a memo to a subject I largely disavow.

I’ll try below to enumerate the macro issues that matter, discuss the outlook for them, and end with some advice regarding what to do about them. That reminds me to put forth my conviction that we all have views about the future, but as we say at Oaktree, “It’s one thing to have an opinion, but something very different to assume it’s right and bet heavily on it.” That’s what Oaktree doesn’t do.

Inflation

As of this writing, macro considerations are certainly in the ascendency, centering on the subject of inflation. Over the last 16 months, the Fed, Treasury and Congress have used a firehose of money to support, subsidize and stimulate workers, businesses, state and local governments, the overall economy and the financial markets. This has resulted in (a) confidence in the prospects for a strong economic recovery, (b) skyrocketing asset prices, and (c) fear of rising inflation.

The policy measures described above traditionally would be expected to produce the following:

a stronger economy than would otherwise have been the case;

higher corporate profits;

tighter labor markets and thus higher wages;

more money chasing a limited supply of goods;

an increase in the rate at which the prices of goods rise (i.e., higher inflation); and, eventually,

a tightening of monetary policy to fight inflation, resulting in higher interest rates.

While the functioning of economies is highly variable and uncertain, economic orthodoxy considers the above process about as reliable as they come. However, I want to take a minute to highlight the uncertainty entailed in thinking about inflation.

Among the defining elements that marked my early years in investing was the 5-15% annual inflation that prevailed in the U.S. from the early 1970s through 1982. Dr. Doom and Dr. Gloom (chief economists Henry Kaufman of Salomon Brothers and Al Wojnilower of First Boston – I forget which was which) regularly admitted in their depressing speeches that they weren’t sure what was causing the inflation or how to bring it down. No one was able to make progress combatting inflation until Fed Chair Paul Volcker solved the problem by raising interest rates dramatically, bringing on a significant double-dip recession in 1980-82.

What about the more recent experience? For years, central bankers in the U.S., Europe and Japan have targeted a healthy 2% rate of inflation, but none of them have been able to produce it. This despite continuous economic growth, significant budget deficits, rapid expansion of the money supply through quantitative easing, and low interest rates – all of which are supposed to be inflationary.

Finally, for roughly the last 60 years, economists have trusted the so-called Phillips Curve, which posits an inverse relationship between unemployment and inflation: the lower the unemployment rate, the tighter the labor market, the more negotiating power workers have, the more wages rise, and the greater the increase in the prices of consumer goods. But the U.S. unemployment rate fell throughout the last decade – ultimately hitting a 50-year low – and still there was no material increase in inflation. Thus, few people talk about the Phillips Curve anymore.

The low reported U.S. inflation rates may be partially attributable to changes in recent decades in the way the Consumer Price Index is calculated, but the truth is that we know very little about inflation, including its causes and cures. I describe it as “mysterious,” so I believe we should put even less stock in predictions surrounding inflation than in other areas. That makes life tough for investors at the moment, because inflation and its impact on interest rates constitute the most important wildcards.

Inflation Outlook Today

There’s been a great deal written about the current prospects for inflation, and rather than rehash it fully, I’ll deliver a brief summary. Here’s the background:

To support the economy and its participants during last year’s Covid-19-related shutdown, the Fed, Treasury and Congress took drastic action to prevent a global slowdown that could have rivalled the Great Depression.

They injected trillions of dollars of liquidity into the economy in the form of benefit payments to individuals, loans and grants to businesses and governments, enhanced unemployment insurance and large-scale bond buying. In fact, I think of 2020 as the year the word “trillions” came into everyday use.

Many people made more money in 2020 than they did in 2019, thanks to the enhanced benefits. 2020’s above-trend incomes coincided with below-trend spending, as we couldn’t take vacations or spend money on dinners, concerts, weddings, etc. The combination of these developments is estimated to have added roughly $2 trillion to consumer balance sheets.

The Fed/Treasury actions flooded the financial markets with money, driving strong price increases and the reopening of the capital markets. The wealth effect – from stock market gains totaling in the double-digit trillions of dollars, plus soaring home prices – was significant; this dwarfed the positive impact on consumer balance sheets of higher incomes and lower spending.

The following signs suggest we may be headed for a significant period of higher inflation:

All the things described immediately above would normally be expected to result in accelerating inflation.

Concern about rising inflation in the next few years has been a topic of elevated discussion. Initially these anxieties were based simply on economic theory, but in 2021 they’ve been supported by empirical evidence:

Used car prices rose dramatically because of shortages of imported parts.

Home prices skyrocketed.

Materials and component prices escalated: e.g., copper, lumber and semiconductors.

Smartphones were in short supply.

Shortages of labor in certain sectors have added to the threat of rising prices.

The year-over-year increase in the Consumer Price Index was 4.2% in April, 5.0% in May and 5.4% in June. These are the highest readings since September 2008.

Not only might higher prices for inputs (“cost-push” inflation) and more dollars chasing goods (“demand-pull” inflation) result in an excess of demand over supply and thus rising inflation, but excessive money printing might reduce the demand for U.S. dollars, cutting the currency’s value and causing the dollar prices of imports to the U.S. to rise.

Particularly troubling in this regard is the recent tendency of those in Washington to spend trillions of dollars without identifying solid “pay-fors.” This has coincided with the rising influence of Modern Monetary Theory, which essentially says deficits and debt don’t matter. What if these ideas are ill-founded?

On the other hand, here are the arguments for why higher inflation might prove “transitory” (the word du jour).

Many of the shortages affecting finished goods and manufacturing inputs – and the resultant price increases – can be seen as a natural consequence of restarting the economy and, especially, the global supply chain. It’s unrealistic to expect all parts of the global economy to immediately resume efficient functioning, and a lack of a single part can cause significant disruption, making it hard to manufacture finished goods. Since these factors result from the restart, they may prove ephemeral.

It should be borne in mind that the prices of raw materials or finished goods aren’t solely determined by current economic developments in a direct, mechanical way, meaning prices aren’t necessarily “right” given prevailing conditions, any more than stock prices are always right. Rather, prices of goods are influenced by economic participants’ psyches and can easily overshoot or undershoot (just as in the stock market). As John Mauldin wrote in Federal Reserve Folly (July 23, 2021), “The rising prices that add up to inflation are the result of producer and consumer expectations for the future.” Thus prices aren’t just the result of supply and demand today, but also an indication of what people think prices will be in the future. We see this in the price of lumber, which rose by roughly 540% between the low in April 2020 – when no one thought there would ever be demand for new homes – and the high in May 2021 – when no one thought the supply of homes could ever meet the demand. Now the price of lumber is down by more than 60% in just the last two months, and we no longer hear much about its contribution to inflation.

Clearly, a lot of the inflation seen in the first half of 2021 can be attributed to increased consumer spending financed by Covid-19 relief and the resultant bulge in savings and wealth. This should prove temporary: a given pool of extra dollars can’t produce elevated spending forever.

The ending of enhanced unemployment benefits in September should bring more workers into the job market, reducing the impact of labor shortages on wages and thus the prices of goods.

The growth of the economy will undoubtedly slow after 2021 or 2022, by which time the impact of 2020’s pent-up consumer demand will ebb significantly.

There’s hope that the recent levels of stimulus, deficit spending and money printing will recede in the next few years (or at least their rate of growth will slow) as the economy continues to expand, meaning these factors will decline relative to the size of the economy.

Technology, automation and globalization are likely to continue to have significant deflationary effects.

The debate rages on regarding whether today’s inflation will prove permanent or transitory. There’s a great deal riding on the answer since higher inflation would doubtless lead to higher interest rates and thus lower asset values. But in my view, it’s impossible to know the answer. (There you have it: important, but not knowable.) There are intelligent people on both sides of the argument, but I’m convinced there’s no such thing as “knowing” what the outcome will be.

What Does the Fed Know?

The Fed is responsible for keeping inflation under control (among its other jobs). However, Fed leaders admit that they’re not highly confident regarding their expectations. Here’s what Fed Chair Jerome Powell said in a June 16, 2021 press conference (emphasis added):

So I can’t give you an exact number or an exact time, but I would say that we do expect inflation to move down. If you look at the forecast for 2022 and 2023 among my colleagues on the Federal Open Market Committee, you’ll see that people do expect inflation to move down meaningfully toward our goal. And I think that the full range of inflation projections for 2023 falls between 2% and 2.3%, which is consistent with our goals.

At roughly the same time, St. Louis Federal Reserve Bank President James Bullard also spoke about the uncertainty that’s present:

Mr. Bullard . . . said the U.S. economy “is in an environment where we’ve got a lot of volatility, so it’s not at all clear that any of this will pan out the way anybody’s talking about.” (The Wall Street Journal, June 18, emphasis added)

This is the kind of candid speech we need. But it’s clear from the above that we can’t conclude “we have the answer” on the subject of inflation . . . or even that there is “an answer.”

What Does the Market Know?

The stock market started off 2016 with a big decline, which seemed to me to be irrational. As a result, I wrote a memo saying the market needed a trip to a psychiatrist (On the Couch, January 14, 2016). The next day, when I went on TV to discuss that memo, I was pressed on whether the stock market’s decline foreshadowed something dire. “No,” I said: the market doesn’t “know” much about the future that we don’t collectively know. That inspired me to write another memo five days later with the same title as this section: What Does the Market Know? (January 19, 2016). What is it telling us today?

In recent months, signs of rapidly rising inflation have been everywhere, and the media have tied the occasional stock market dips to inflation fears. For example, the S&P 500 Index experienced a moderate decline for the 10 trading days ending on June 18. Here’s what The Wall Street Journal had to say the next day:

U.S. stocks retreated Friday, as traders warily eyed the Federal Reserve for hints of where monetary policy is headed.

The Dow Jones Industrial Average had its worst week since the week ended Oct. 30. The index of blue-chip stocks on Friday fell 1.6%, or 533.37 points, to 33290.08. For the week, it lost 3.45%.

The S&P 500 declined 1.3%, or 55.41 points, to 4166.45 on Friday, losing 1.9% on the week. That broke a three-week streak of gains. The Nasdaq Composite lost 0.9%, or 130.97 points, to 14030.38, as large technology stocks also fell. For the week, it was down 0.3%.

Policy makers had signaled Wednesday that they expect to raise interest rates by late 2023, sooner than they had previously anticipated. Sentiment waned again on Friday after Federal Reserve Bank of St. Louis leader James Bullard said on CNBC that he expects the first rate increase even sooner, in late 2022. . . .

It isn’t surprising that equities are falling, said ThinkMarkets analyst Fawad Razaqzada. U.S. stocks have hit a series of record highs and have been outpacing the economic recovery since last year. Now traders are repricing that “reflation trade” as they watch the Federal Reserve slowly start to alter its stance on monetary policy.

“It was coming,” he said. “This kind of selloff was coming because the market got ahead of itself.”

The Cboe Volatility Index, known as Wall Street’s “fear gauge,” climbed to its highest level in weeks.

“The markets will be more spooked by 2022 turning to a rate hike, because that will mean they have to taper as well,” said Derek Halpenny, head of research for global markets in the European region at MUFG Bank. (The Wall Street Journal, June 19)

As usual, media commentators stand ready to explain in a logical fashion why the markets did what they did (I always wonder where they look to get the explanation). They’re also glad to tell us what that means for the future, invariably through extrapolation.

Regardless, the theme thus far in 2021 has been rising inflation. That and the associated fear of higher interest rates have been used to explain much of what’s been going on in the stock market. The data reflected rapidly rising inflation, and stock market investors turned negative.

So far, so good. You might say the stock market was efficiently reflecting developments and the outlook. But the bond market didn’t see it the same way:

In bond markets, the yield on the 10-year Treasury note fell to 1.449% Friday, down from 1.509% Thursday. The 10-year yield has fallen for five straight weeks . . .

Consumer prices paid by city dwellers in the U.S. rose more than 7% [in May] and more than 9% in April on an annualized basis. If this keeps up the rest of the year, it will be the highest inflation rate the U.S. has experienced since the 1980s. But fear not, say some investors and the Federal Reserve, the bond market isn’t worried. Yields fell over the last week and remain low by historical levels, even after rising on the back of [Fed Chair] Jay Powell’s speech Wednesday. And if markets aren’t worried, maybe we shouldn’t be either. . . . (Allison Schrager, senior fellow at the Manhattan Institute, Bloomberg Opinion, June 18)

The stock market was afraid of higher inflation and interest rates, but the bond market – where price movements are governed predominantly by the outlook for rates – gave us higher prices and lower rates, seemingly unconcerned about inflation.

That brings me to gold, which historically has been bought for protection against inflation. Despite all the inflationary signs, the market for gold seems to agree with the bond market that the outlook for inflation is benign.

Gold futures fell 0.3%, adding to their losses from Thursday, when they suffered their largest drop in over 10 months. For the week, gold fell 5.8%, its worst one-week performance since the week ended March 13, 2020. (The Wall Street Journal, June 19)

The price of gold hit an all-time high of $2,067 per ounce on August 6, 2020, likely driven by the Fed’s enormous injection of money into the economy and markets. And then, on June 18, 2021, when concern about inflation seemed to be rising, it hit $1,773, down 14% from the high reached 10 months earlier. (Gold prices from Goldhub)

So in June we had bouts of stock market weakness, reportedly on inflation fears, and rising bond prices (declining yields), seemingly based on bond buyers’ conviction that economic weakness will keep inflation subdued. And we saw gold, the classic anti-inflation tool, marked down just as stock market investors were described as being concerned about inflation. Not only do the markets not know what’s coming, but they often behave in ways that make little or no long-term sense.

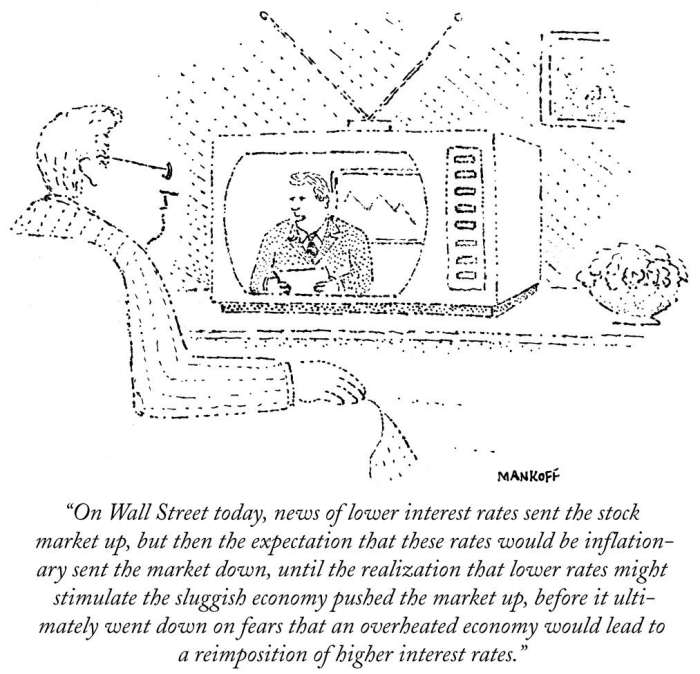

I concluded my 2016 memo What Does the Market Know? by saying that, on the subject of when to buy and sell securities, “the market has nothing useful to contribute.” I think we can say the same about what it knows about future macro events. Perhaps the market’s thought process is best understood through this old cartoon – one of the greatest of all time – which I included in On the Couch.

Markets function like highly sensitive instruments, absorbing events and publishing their reaction, be it bullish or bearish. While markets are usually good “observers,” hyper-attuned to current developments, they sometimes seem to view events through either a positive or a negative lens (and to oscillate between the two), as shown above. Further, they’re rarely good “predictors,” in the sense of knowing what comes next.

Because their reaction to short-run developments tends toward excess, the markets provide a lot of false positives and negatives regarding their significance. But the fact that markets can overemphasize current developments and fail to look far enough into the future doesn’t mean they should be ignored entirely. In particular, when security prices perform differently than what we would expect based on our views, we should consider whether the market has discerned something that throws our prior understanding into question. (Are the markets capable of exceptional insight? Check out the S&P 500’s 68% gain from its low on March 23 through the end of 2020, which “no one” thought made sense when it began. The markets certainly did a much better job of recognizing the potential impact of the Fed/Treasury actions than did most commentators.)

What Do the Forecasters Know?

Although it’s on the subject of stock market returns rather than inflation, I can’t fail to share some data regarding forecasts supplied by Sheldon Stone, my longest-running partner (we just passed 38 years working together). Last December, he shared a New York Times article by Jeff Sommer entitled “Clueless About 2020, Wall Street Forecasters Are at It Again for 2021” (December 18, 2020). According to the article:

In December 2019, the median forecast on Wall Street held that the S&P 500 would rise 2.7% in 2020. Since the actual return on the index was 18.4%, that forecast was too low by 16 percentage points. But in April 2020, after the pandemic had taken hold (and after the initial actions on the part of the Fed, Treasury and Congress had been announced and initiated), the consensus forecast return was revised downward to negative 11% – almost 30 percentage points below the eventual outcome.

Obviously, nobody could have been expected to have predicted the pandemic. Ditto for the full success of the policy response or the timing and extent of the consequent market bounce. But Sommer shared longer-term data from Paul Hickey, co-founder of Bespoke Investment Group, which is more meaningful. I’ll mostly use Sommer’s words to convey the facts:

Since 2000, the median analyst forecast has called for an average yearly return on the S&P 500 of 9.5%, whereas the actual average gain was 6.0%. You might say, “not bad, only off by 3.5 percentage points.” Or you might say, “terrible – the forecasters overestimated the average gain by 58% (9.5/6.0 - 1).”

“Each December since 2000, the median forecast never called for a stock market decline over the course of the following calendar year . . .” (emphasis added). And yet the stock market lost money in six of those years.

“In 2018, for example, the market fell 6.9 percent, though the forecasters said it would rise 7.5 percent, a spread of 14.4 percentage points. In 2002, the forecast called for an increase of 12.5 percent, but stocks fell 23.3 percent, a spread of almost 36 percentage points.”

“All told, when gaps like that are taken into account, the median Wall Street forecast from 2000 through 2020 missed its target by an average 12.9* percentage points — which was more than double the [6.0%] actual average annual performance of the stock market. Year after year, these forecasts are about as accurate as those of a weatherman who always calls for balmy sunshine in a city where it rains or snows about 30 percent of the time. Some forecasts!” (* What accounts for the difference between the average error of 3.5 percentage points cited in the first bullet point and this 12.9? I assume the latter to be the average of the “absolute value” of the error. When you think in terms of absolute value, being too high by 3% in year one and then too low by 2% in year two means the absolute values of the errors add up to 5%, rather than netting out to only 1%.)

The bottom line is that hundreds or perhaps thousands of people make their living as professional market forecasters, despite the fact that the median forecast is of no value: wrong on average, positive in good years and bad, and way off target when an accurate forecast would have been most profitable.

The Role of the Fed

A great deal of the current debate over the macro outlook surrounds the Fed and its policies and behavior. In March 2020, the Fed triggered the recovery we’re enjoying by cutting the key federal funds rate to 0-0.25%, initiating loan and grant programs, and buying vast amounts of bonds. This combination was very successful, producing powerful recoveries in the economy and the financial markets. However, the same actions helped create the threat of persistently higher inflation.

The Fed has two primary assignments: (a) making sure the economy grows enough to create jobs, leading to full employment, and (b) keeping inflation under control. To some extent, these tasks are in conflict. Stronger economic growth risks overheating and inflation. Higher inflation leads investors to demand higher interest rates to more than compensate for the loss of purchasing power. Higher interest rates threaten to slow the economy.

The economic outlook turned positive last summer in response to the Fed/Treasury actions and then was further bolstered by the success of vaccines. Thus, we’re seeing strong economic growth – real GDP rose at an annualized rate of 6.4% in the first quarter – and expectations remain high for the rest of 2021 and perhaps 2022. Yet, the Fed continues to hold interest rates near zero and buy $120 billion of bonds per month. Why stimulate an economy that’s doing so well, and run the risk of inflation?

In fact, the Fed seems to be relatively unworried about inflation. At first it said it didn’t think there would be inflation (recent data has disproved that). Then it said if there is inflation, it will be transitory. And the Fed went on to say if inflation appears to be other than transitory, they have the tools with which to fight it.

By maintaining its high level of accommodativeness, the Fed is showing that it’s more worried about economic sluggishness than about inflation. One informed observer told me that if growth falls back to the recent norm of 2% or less despite all the stimulus that’s been thrown at the economy, the Fed feels we risk serious stagnation. And let’s remember that (a) ever since the turn of the century there has been slow GDP growth and serious discussion of “secular stagnation” and (b) while the economic recovery from 2009 through 2019 was the longest in history, it was also the slowest since World War II.

Fed Chair Powell’s recent testimony shows how he prioritizes the considerations, several months into the recovery:

Federal Reserve Chair Jerome Powell on Wednesday pledged “powerful support” to complete the U.S. economic recovery from the coronavirus pandemic . . .

In testimony to the U.S. House of Representatives Financial Services Committee, Powell said he is confident recent price hikes are associated with the country's post-pandemic reopening and will fade, and that the Fed should stay focused on getting as many people back to work as possible.

Any move to reduce support for the economy, by first slowing the U.S. central bank’s $120 billion in monthly bond purchases, is “still a ways off,” Powell said, with 7.5 million jobs still missing from before the pandemic. (Reuters, July 14)

But even if economic sluggishness is the greater risk – and who’s to disagree with the Fed and insist it’s not – the risk of inflation is still real, as would be the consequences. I’m sure we’re all much better off with the Fed possibly overshooting on stimulus, rather than undershooting. And I believe the Fed was right to do all it did despite the possibility of negative ramifications. Still, we must consider those ramifications.

Higher inflation could lead to higher interest rates as investors demand positive real yields, but also if tighter monetary policy and higher rates are employed to fight the inflation.

Higher interest rates could negatively affect the economy.

Higher interest rates make investors demand higher returns, leading to lower prices for financial assets and the possibility of a market collapse (see 1972-82).

Higher inflation would hit low-income Americans the hardest, since they spend the lion’s share of their incomes on necessities, and threaten the lifestyle of the millions of retirees and others on fixed incomes.

Higher interest rates would raise the cost of servicing the national debt, further swelling the annual deficits (and therefore the national debt).

Larger deficits could make lenders (and foreign buyers) demand still-higher interest rates on U.S. debt securities, creating a negative feedback loop.

If we continue to print enough money to pay the interest and fund the deficit, eventually the value of the dollar and its use as the world’s reserve currency could be called into question.

As we’ve experienced in the past, rapidly rising prices could cause inflationary expectations to become embedded in Americans’ psyches, making the increases self-perpetuating and hard to combat.

Further, we should consider the negative aspects of accommodative monetary policy itself:

Fed largesse can be viewed as implying the existence of a “Fed put,” or a guarantee of future bailouts. The consequences can include increased moral hazard (the belief that investors can take risk without consequences) and a diminution of the risk aversion that must be present in order for markets to be safe.

The above conditions can lead businesses and investors to use more leverage, magnifying the potential damage from a slowdown.

As we’ve seen in the last 16 months, the Fed can’t stimulate the economy without increasing the value of the economy. And who receives the benefit? The people who own the economy (i.e., the owners of equities, companies and real estate). Thus, stimulus and the resultant asset appreciation exacerbate the disparity in wealth, which is receiving increased consideration.

If the Fed maintains its current level of accommodation – including keeping interest rates near zero – it will have relatively few levers to pull in case a future slowdown calls for incremental stimulus. For example, cutting interest rates was a key part of last year’s rescue package. This wouldn’t have been possible if rates had been at zero when the Fed first took action.

Some people wonder whether the Fed might produce perpetual prosperity, preventing recessions or minimizing them as it did last year. Some hope low interest rates can keep markets aloft forever. Some think the Treasury can issue as much debt as is needed, with the Fed willing to step in as the buyer of last resort. Obviously, a lot of people in the federal government think unlimited sums can be spent without negative consequences from the resulting increased deficits and debt.

I’m not smart enough to prove it, but to me these assumptions seem too good to be true. They have the appearance of a perpetual motion machine or a credit card with no credit limit and no requirement to pay off the balance. I can’t tell you exactly what the catch is, but I think there has to be one. Or, perhaps better put, I wouldn’t bet the ranch on there not being a catch.

In the 1930s, John Maynard Keynes suggested that nations should run fiscal deficits in times of weakness to stimulate demand, reenergize their economies, and create needed jobs. It’s not for nothing that deficit spending is described as “Keynesian.” But even Lord Keynes asserted that while deficits are a reasonable way to jumpstart a sluggish economy, governments should run surpluses in times of prosperity and use them to repay the debts incurred in times of weakness. However, in the 21st century, concepts like fiscal discipline, budget surpluses and debt repayment seem to have gone out the window.

The U.S. has run large and growing deficits for more than 20 years, and that seems less likely than ever to change. Traditional economics asserts that this will be inflationary, but as mentioned earlier, the deficits of the 2010s didn’t bring on substantial inflation. Perhaps they merely helped support an economy that would have been even weaker in their absence.

Regardless, we’ve now entered into a time of testing. As I said earlier, in 2020, we saw trillions of dollars of increased benefits, Fed bond-buying, expansion of the Fed balance sheet, federal fiscal deficits, and additions to the U.S. national debt. All of these things increased sharply as a percentage of the total economy. We’ll see the consequences in the future.

Alan Greenspan made the Fed highly activist starting in the 1990s (giving rise to the concept of the “Greenspan put” and eventually the “Fed put”), a posture that has persisted through three financial crises already in this young century. Again, the Fed’s rescue actions have been essential and appropriate, but in my view they should not be permanent. I would prefer to see a Fed that isn’t continually fine-tuning, but rather one taking a “hands-off” approach most of the time and acting to stimulate or restrict the economy only at extremes.

I imagine my readers believe in the free market and, especially, its power as the best allocator of resources. In a free market, Adam Smith’s “invisible hand” moves resources such as labor and capital where they can be most productive. But we don’t have a free market in money today, and we haven’t had one since at least 2008’s Global Financial Crisis; the Fed cut the federal funds rate to zero in January 2009 and has kept it low ever since. There have been attempts to raise interest rates, but the markets greeted them with a series of “tantrums,” discouraging continued efforts.

I want to make clear that I don’t think I know better than the people who run the Fed. However, in general, I would like to see the economy stimulated less often, and certainly not continually. We might like to have faster growth in the years ahead than the economy would provide on its own, but I don’t think the long-term rate of growth can be lifted perpetually through monetary and fiscal policy, and certainly not without the risk of negative consequences.

To have a healthier allocation of capital, I’d like to see a free market in money, and to me that means interest rates that are “naturally occurring.” Rates held artificially low distort the capital markets, penalizing savers, subsidizing borrowers, lifting asset prices and encouraging increased risk taking and the use of more leverage. Again, I’d prefer to see a Fed that’s reluctant to intervene other than when intervention is essential.

* * *

In my first memo of the pandemic, I wrote the following about the coronavirus:

No one knows much about it, since this is its first appearance. As Harvard epidemiologist Marc Lipsitch said on a podcast on the subject, there are (a) facts, (b) informed extrapolations from analogies to other viruses and (c) opinion or speculation. The scientists are trying to make informed inferences. Thus far, I don’t think there’s enough data regarding the coronavirus to enable them to turn those inferences into facts. (Nobody Knows II, March 3, 2020)

Substitute “economists” for “scientists” and “inflation” for “coronavirus,” and I think this paragraph can serve well today. In thinking about the causes of inflation, there are few facts and only one prior inflationary episode in the U.S. in our lifetimes from which to extrapolate. Thus, I consider anything anyone says today about inflation in the coming years to be Lipsitch’s “opinion or speculation” . . . or, as I’d say, “guesswork.”

I’ve written in the past about the way I tend to come across great material just as memos are approaching the finish line. Thus, I want to include a quote that connects with Lipsitch’s view. It’s from Bill Miller, a legendary investor with an outstanding record:

No one has privileged access to the future and market forecasts tend to be about as accurate as calling a coin toss. There are, of course, analogies that can be drawn about how the current environment maps onto previous historical data, but success in that depends crucially on how the future will, in fact, resemble the past, and whether the cited analogies turn out to be the governing ones. The record seems to show that sometimes they will and sometimes they won’t and we are back at the coin toss. (Bill Miller 2Q 2021 Market Letter, July 9, 2021)

The following quote does a terrific job of summarizing the challenge entailed in decision-making in cases like this:

No amount of sophistication is going to allay the fact that all your knowledge is about the past and all your decisions are about the future. (Ian H. Wilson, former GE executive)

That doesn’t mean people won’t express forceful opinions regarding inflation in the period ahead. As I wrote 17 years ago:

“Confident” is the key word for describing members of [the “I know”] school. For the “I don’t know” school, on the other hand, the word – especially when dealing with the macro-future – is “guarded.” Its adherents generally believe you can’t know the future; you don’t have to know the future; and the proper goal is to do the best possible job of investing in the absence of that knowledge. (Us and Them, May 7, 2004)

So what does that mean for investor behavior today? If we can’t know whether today’s inflation will prove transitory or be with us for a while, is there nothing for investors to do? The answer lies in the title of a 2001 memo of mine:You Can’t Predict. You Can Prepare. No one can confidently predict whether we’re entering an inflationary era, but the consequences of doing so would be significant. Thus, I’ll briefly rehash the opinion regarding market exposure that I expressed in my review of 2020.

In January’s memo Something of Value, I described the way my genetic makeup, early experiences, and success in blowing the whistle on some unsustainable financial innovations and market excesses had turned me into something of a knee-jerk skeptic. My son Andrew called this to my attention while our families lived together last year, and what he said struck a responsive chord.

The old me likely would have latched onto today’s high valuations and instances of risky behavior to warn of a bubble and the subsequent correction. But looking through a new lens, I’ve concluded that while those things are there, it makes little sense to significantly reduce market exposure:

on the basis of inflation predictions that may or may not come true,

in the face of some very positive counterarguments, and

when the most important rule in investing is that we should commit for the long run, remaining fully invested unless the evidence to the contrary is absolutely compelling.

Finally, I want to briefly touch on the level of today’s markets. Over the four or five years leading up to 2020, I was often asked whether we were in a high yield bond bubble. “No,” I answered, “we’re in a bond bubble.” High yield bonds were priced fairly relative to other bonds, but all bonds were priced high because interest rates were low.

Today, we hear people say everything’s in a bubble. Again, I consider the prices of most assets to be fair relative to each other. But given the powerful role of interest rates in determining those prices, and the fact that interest rates are the lowest we’ve ever seen, isn’t it reasonable that many asset prices are the highest we’ve ever seen? For example, with the p/e ratio of the S&P 500 in the low 20s, the “earnings yield” (the inverse of the p/e ratio) is between 4% and 5%. To me, that seems fair relative to the yield of roughly 1.25% on the 10-year Treasury note. If the p/e ratio were at the post-World War II average of 16, that would imply an earnings yield of 6.7%, which would appear too high relative to the 10-year. That tells me asset prices are reasonable relative to interest rates.

Of course, it’s one thing to say asset prices are fair relative to interest rates, but something very different to say rates will stay low, meaning prices will stay high (or rise). And that leads us back to inflation. It isn’t hard to imagine rates increasing from here, either because the Fed lifts them to keep the economy from overheating or because rising inflation requires higher rates in order for real returns to be positive (or both). While the possibility of rising rates (and thus lower asset prices) troubles us all, I don’t think it can be said that today’s asset prices are irrational relative to rates.

Whereas folks from the media try to get me to say “buy” or “sell” and “in” or “out,” I formulate my view nowadays in terms of the appropriate mix of aggressiveness versus defensiveness. Given the above crosscurrents, Oaktree is maintaining a balance between the two that’s generally in line with our normal stance (as opposed to the elevated defense we maintained going into 2020).

Having said that, it’s reasonable to make some adjustments at the margin in response to the risk of inflation. Investors who feel strongly about the risk, or who worry more about interim markdowns (and less about gains they might forgo if inflation fails to materialize), might wish to emphasize:

floating-rate debt;

investments in businesses with largely fixed costs or the ability to pass on cost increases, or that can otherwise incorporate inflation in prices (like certain landlords); and/or

situations where profits have the potential to grow faster than prices rise.

These are all ways one might prepare today for an inflationary environment. I consider it reasonable for investors to give a nod to the possibility of higher inflation, but not to significantly invert asset allocations in response to macro expectations that may or may not prove accurate.

July 29, 2021

LEGAL INFORMATION AND DISCLOSURES

This memorandum expresses the views of the author as of the date indicated and such views are subject to change without notice. Oaktree has no duty or obligation to update the information contained herein. Further, Oaktree makes no representation, and it should not be assumed, that past investment performance is an indication of future results. Moreover, wherever there is the potential for profit there is also the possibility of loss.

This memorandum is being made available for educational purposes only and should not be used for any other purpose. The information contained herein does not constitute and should not be construed as an offering of advisory services or an offer to sell or solicitation to buy any securities or related financial instruments in any jurisdiction. Certain information contained herein concerning economic trends and performance is based on or derived from information provided by independent third-party sources. Oaktree Capital Management, L.P. (“Oaktree”) believes that the sources from which such information has been obtained are reliable; however, it cannot guarantee the accuracy of such information and has not independently verified the accuracy or completeness of such information or the assumptions on which such information is based.

This memorandum, including the information contained herein, may not be copied, reproduced, republished, or posted in whole or in part, in any form without the prior written consent of Oaktree.

We use cookies to provide the best user experience. By continuing to browse this website, you will be considered to accept cookies. Please review our Privacy Policy to learn our cookie policy.

Shipping & ShipbuildingHanwha Ocean shares sink after KDB's sale of 4.2% stake

Shipping & ShipbuildingHanwha Ocean shares sink after KDB's sale of 4.2% stake EnergySouth Korea nears Czech nuclear deal; Doosan, related stocks fly high

EnergySouth Korea nears Czech nuclear deal; Doosan, related stocks fly high

Business & PoliticsSeoul, Washington agree on July tariff deal framework in '2+2' trade talks

Business & PoliticsSeoul, Washington agree on July tariff deal framework in '2+2' trade talks