Banks in pandemic era

Tight margins, regulatory meddling weigh on Korean banks

By Feb 08, 2021 (Gmt+09:00)

4

Min read

Most Read

LG Chem to sell water filter business to Glenwood PE for $692 million

KT&G eyes overseas M&A after rejecting activist fund's offer

Mirae Asset to be named Korea Post’s core real estate fund operator

StockX in merger talks with Naver’s online reseller Kream

Meritz backs half of ex-manager’s $210 mn hedge fund

Looking ahead, stagnant or falling non-interest incomes and big tech firms’ advance into financial services weigh on their outlook, coupled with an increase in provisioning costs expected in the prolonged pandemic era. Further, higher levels of regulatory meddling means they have less leeway in lending and dividend policies, hampering their efforts to return profits to shareholders.

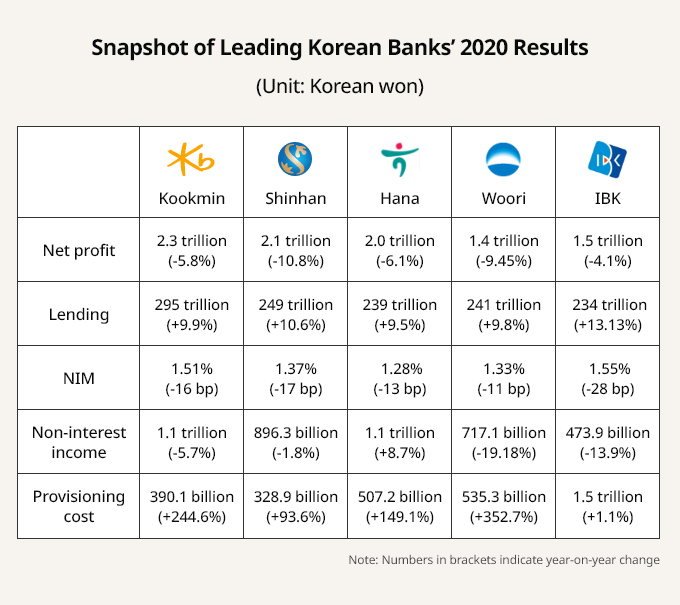

Net profits at the five South Korean banks – Kookmin, Shinhan, Hana, Woori and Industrial Bank of Korea (IBK) – declined by 4-11% last year from a year earlier, despite a 10% rise in lending on average. It was the first time their net profits saw a year-on-year drop since 2015.

“2015 was the last year that banks set aside heavy provisioning to brush off losses stemming from the shipbuilding and shipping industries in the wake of the global financial crisis,” said a banking official. “Having posted steady growth since then, the banking industry is now at an inflection point due to ultra-low interest rates and the COVID-19 fallout.”

Net interest margins (NIM) at all the five banks contracted more than 10 basis points last year, with Shinhan Bank’s NIM shrinking by 17 basis points to 1.37%. The Bank of Korea’s benchmark rate cut to a record low of 0.5% last year further squeezed banks’ lending margins.

Non-interest incomes shrank as well, excluding Hana Bank.

“After the fund scam scandals, customers became reluctant to buy funds. They are now turning direct investors, making it hard to sell funds,” said another domestic bank official. He referred to a series of fraud scandals involving domestic financial services firms last year. Investors in the funds have yet to retrieve several billions of dollars they are owed.

Bracing for the accelerating digital transformation amid the contactless trend, the leading Korean banks, excluding state-run IBK, let go of a large number of employees under voluntary retirement programs last year. That resulted in heavy one-off charges. Woori Bank reported a 352.7% surge in its year-on-year provisioning costs.

As regards to 115 trillion ($103 billion) in loans owed by those hit hard by the pandemic, domestic banks extended their maturity date to March of this year. The loans are likely to be rolled over again, while they were classified as normal loans as of Dec. 14, 2020.

“Thanks to rising market interest rates, we have room to improve profitability. But the biggest concern is that we may have to increase provisioning following the annual credit assessment of companies in May and June,” a Korean bank CEO told The Korea Economic Daily.

REGULATORY RECOMMENDATIONS

The 2020 results of the Korean lenders contrasted with those of their parent holding groups, which enjoyed a bumper year for earnings, benefiting from the stock markets’ bull run.

Despite their record earnings, the country’s financial regulators advised the financial holding groups to restrict dividend payments to less than 20% of their net profits to buffer the effects of the global pandemic. KB Financial Group and Hana Financial Group lowered dividend payouts to 20% from the previous year’s 26%, as advised, while Shinhan and Woori have not yet decided on dividend payments.

“That’s not legally binding, but if we go far beyond the recommendation, we may find it difficult to communicate with the regulatory authorities in the future,” Shinhan Financial Group’s Chief Financial Officer Roh Yong-hoon told a quarterly conference call on Feb. 5. Last year, Shinhan Financial Group Chairman Cho Yong-byoung had vowed to share more profits with shareholders, including paying hefty dividends.

Adding further pressure, the regulatory Financial Supervisory Service recently notified the chairmen of Woori and Shinhan financial groups and Shinhan Bank CEO Jin Ok-Dong of its plan to reprimand them regarding their companies' sale of investment funds involved in the fraud scandals.

Additionally, domestic banks are required to donate part of their earnings to funds set up to help the victims of COVID-19, while reducing loans to individuals as part of government efforts to cool the overheated residential real estate market.

“It’s been several months since the authorities called for curbing credit loans, while telling us to increase lending to the victims of COVID-19,” said another banking industry official.

Write to So-ram Jung and Dae-hun Kim at daepun@hankyung.com

Yeonhee Kim edited this article.

More to Read

-

Business & PoliticsTrump Jr. meets Korean business chiefs in back-to-back sessions

Business & PoliticsTrump Jr. meets Korean business chiefs in back-to-back sessionsApr 30, 2025 (Gmt+09:00)

-

Korean chipmakersSamsung in talks to supply customized HBM4 to Nvidia, Broadcom, Google

Korean chipmakersSamsung in talks to supply customized HBM4 to Nvidia, Broadcom, GoogleApr 30, 2025 (Gmt+09:00)

-

EnergyLS Cable breaks ground on $681 mn underwater cable plant in Chesapeake

EnergyLS Cable breaks ground on $681 mn underwater cable plant in ChesapeakeApr 29, 2025 (Gmt+09:00)

-

Business & PoliticsUS tariffs add risk premium to dollar assets: Maurice Obstfeld

Business & PoliticsUS tariffs add risk premium to dollar assets: Maurice ObstfeldApr 29, 2025 (Gmt+09:00)

-

Comment 0

LOG IN