Market Watch

Korean household credit risk nears record-high

By Jul 16, 2020 (Gmt+09:00)

3

Min read

Most Read

LG Chem to sell water filter business to Glenwood PE for $692 million

Kyobo Life poised to buy Japan’s SBI Group-owned savings bank

KT&G eyes overseas M&A after rejecting activist fund's offer

StockX in merger talks with Naver’s online reseller Kream

Mirae Asset to be named Korea Post’s core real estate fund operator

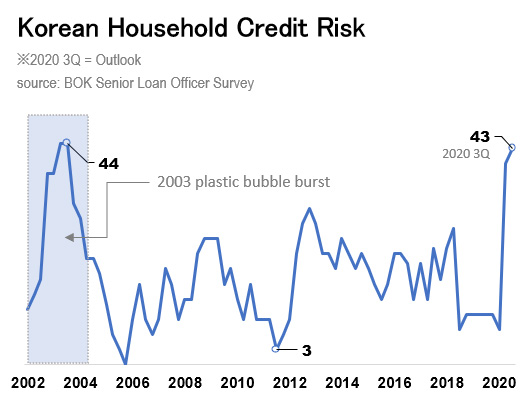

Korea's household credit risk hit the second-highest record for the upcoming third quarter, driven by impacts of the global pandemic which has reduced income for many households struggling with debt.

On July 13, Bank of Korea released a ‘Senior Loan Officer Opinion Survey on Bank Lending Practices’ which placed the third quarter (July to September period) household credit risk index at 43. The index range is set between minus 100 and 100, with the number edging closer to 100 if there are more predictions of increased risk compared to reduced risk against the previous quarter.

This is the second-highest figure since reaching an all-time high index value of 44 during the third quarter of 2003, 17 years ago when Korea was hit by the credit card bubble, also referred to as the plastic bubble.

In 1999, the Korean government lifted the cash advance limit of 700,000 won ($582) to promote the use of credit cards. This led to people taking out excessive cash advances, as well as credit card companies recklessly issuing cards to students and unemployed people without checking their credit ratings or reviewing their ability to make payments.

Cash advance fees were around a high 20%, but this did little to deter users as it provided cash quickly and easily. Many households began to open numerous credit cards to take out loans and use it for their business funds as well as living expenses. Often borrowers overspent and took out card loans and cash advance which exceeded their income.

The 48 trillion won worth of cash advance in 1999 surged to 358 trillion won in 2002, more than seven times in just three years.

Starting in 2002, the government began to enforce tighter rules to prevent minors from opening credit cards and lowered the cash advance limit - but it was too late. Already many households and self-run businesses were unable to pay off the massively accrued amount of principal and interest. As a result, credit card companies found themselves in trouble, with some going nearly bankrupt and having to undergo corporate restructuring.

KB Card and Woori Card merged into their parent bank holding companies to survive. Samsung Group injected 5 trillion won to salvage Samsung Card, and LG Card, the industry’s leading credit card company at the time, terminated cash advance services and was sold off by LG Group to be eventually merged with Shinhan Card.

The current situation may not seem similar to the 2003 credit card bubble given that the default rate released by financial institutions is not high. However, it is too soon to be assured by low default rates when considering the survey results from financial managers. This is because principals are often paid with new debt when it is easy to borrow cash at a low-interest rate, like nowadays.

Even in 2001, just two years prior to the 2003 credit card bubble, card companies' default rate was at a historic low which was disrupted shortly with a full-blown liquidity crisis.

“Loan managers expect to see increased credit risk among vulnerable borrowers such as low-credit, low-income class due to their inability to make repayments,” according to Bank of Korea which conducted the survey across 199 financial institutions.

If Korea's household credit worsens to the likes of 2003, then the result could be devastating.

There were near 3.72 million credit card delinquents (unpaid principal for over three months) at the end of 2003, accounting for almost 16% of the economically active population of 22.9 million. As a result, the GDP growth rate plummeted to 3.1%, half of the previous year’s 7.7%, according to the Korea Federation of Banks.

Write to Taeho Lee at thlee@hankyung.com

Danbee Lee edited this article

More to Read

-

Shipping & ShipbuildingHanwha Ocean shares sink after KDB's sale of 4.2% stake

Shipping & ShipbuildingHanwha Ocean shares sink after KDB's sale of 4.2% stakeApr 29, 2025 (Gmt+09:00)

-

EnergySouth Korea nears Czech nuclear deal; Doosan, related stocks fly high

EnergySouth Korea nears Czech nuclear deal; Doosan, related stocks fly highApr 25, 2025 (Gmt+09:00)

-

-

Business & PoliticsSeoul, Washington agree on July tariff deal framework in '2+2' trade talks

Business & PoliticsSeoul, Washington agree on July tariff deal framework in '2+2' trade talksApr 25, 2025 (Gmt+09:00)

-

Comment 0

LOG IN