Korean rating agency warns of fast alternative asset growth, resale risk

Sep 28, 2019 (Gmt+09:00)

LG Chem to sell water filter business to Glenwood PE for $692 million

Kyobo Life poised to buy Japan’s SBI Group-owned savings bank

KT&G eyes overseas M&A after rejecting activist fund's offer

StockX in merger talks with Naver’s online reseller Kream

Mirae Asset to be named Korea Post’s core real estate fund operator

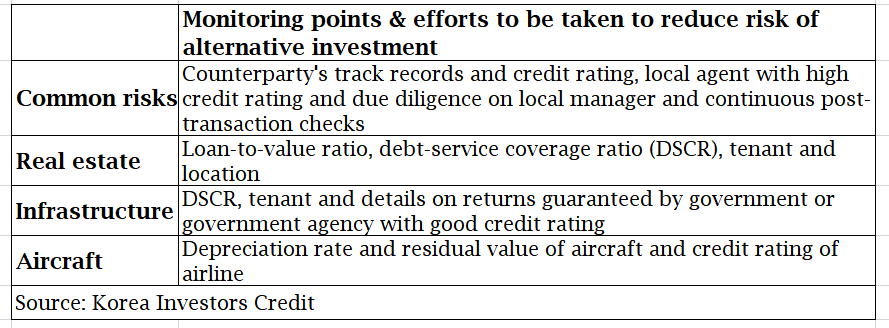

The pace of growth in overseas alternative investments by South Korean securities companies has been “too rapid” over the past 18 months and brought their liquidity risk to the fore because of a growing risk of resale failure, Korea Investors Service (KIS) said in a recent report.

The outstanding balance of cross-border alternative investments at eight Korean securities firms more than trebled to 13.9 trillion won ($11.6 billion) as of end-June 2019, compared with 3.7 trillion won at the end of 2017.

Of the total, 1.3 trillion won ($1.1 billion) worth of investments have been left in the hands of the brokerage firms for more than six months, with real estate in Europe making up the bulk of the unsold assets, said KIS, part of Moody’s Investors Service, on Sept. 25.

“Because of excessive competition, the risk of resale failure is growing. If the current investment trends continue, securities companies will end up with liquidity deterioration and investment losses,” the agency said in the report, entitled “Surging overseas alternative investment: risks in the securities and insurance sectors?”

“Recently, securities companies are increasing borrowing at a rapid pace and their contingent liabilities are increasing, too.”

Going forward, domestic brokerage firms will continue to chase high-yielding assets, with global alternative investment market projected to reach $14 trillion in 2023, it added.

Their exposure to cross-border alternative investments remains moderate at 38% against capital, compared with 26% for insurers, but the exposure growth was too rapid.

Further, they have been piling into subordinated debt and equity tranches in real estate and infrastructure assets for better yields, while diversifying beyond developed markets and office buildings, it cautioned.

Behind the surging alternative investments were a relaxation in net capital ratio rules for domestic brokerage companies effective from 2016 and policy support for so-called “super-sized investment banks” with an equity capital of at least 4 trillion won.

Their overseas alternative portfolios consist of principal investment and sell-down assets at 49.6% and 50.4%, respectively.

“If the increased investment in long-term assets, resale failure and contingent liabilities growth deteriorate their liquidity conditions, we will reflect them in the evaluation of their credit risks.”

By region, US and Europe accounted for 43.4% and 32.4% of overseas alternative investments at eight securities and 10 insurance companies, on which the research was based. It was presented during the KIS' second-half seminar.

Infrastructure and real estate accounted for a majority of the alternative portfolios, about 40% of which are expected to yield 6-8% per annum, according to the report.

The report was published after Mirae Asset Financial Group signed an agreement in early September to buy a portfolio of 15 US luxury hotels from Anbang Insurance Group for $5.8 billion. Brokerage unit Mirae Asset Daewoo Co. Ltd. is expected to take a big chunk of the acquisition financing.

KIS has not taken any rating action on domestic securities firms yet in relation to alternative investments.

Meanwhile, 10 insurance companies in Korea have raised exposure gradually to overseas alternatives to 15.4 trillion won as of end-June, versus 10.5 trillion won at end-2017.

In aggregate, overseas alternative investment funds in South Korea have soared by 38% CAGR to 104 trillion won ($87 billion) over the past 10 years, KIS said.

Yeonhee Kim edited this article

-

Real estateMirae Asset to be named Korea Post’s core real estate fund operator

Real estateMirae Asset to be named Korea Post’s core real estate fund operatorApr 29, 2025 (Gmt+09:00)

-

Asset managementMirae Asset bets on China as Korean investors’ US focus draws concern

Asset managementMirae Asset bets on China as Korean investors’ US focus draws concernApr 27, 2025 (Gmt+09:00)

-

Alternative investmentsMeritz backs half of ex-manager’s $210 mn hedge fund

Alternative investmentsMeritz backs half of ex-manager’s $210 mn hedge fundApr 23, 2025 (Gmt+09:00)

-

Real estateRitz-Carlton to return to Seoul, tapped by IGIS Asset for landmark project

Real estateRitz-Carlton to return to Seoul, tapped by IGIS Asset for landmark projectApr 22, 2025 (Gmt+09:00)

-

Real estateS.Korean gaming giant Netmarble eyes headquarters building sale

Real estateS.Korean gaming giant Netmarble eyes headquarters building saleApr 18, 2025 (Gmt+09:00)