Memo from Howard Marks

Fewer losers, or more winners?

Sep 22, 2023 (Gmt+09:00)

long read

Most Read

LG Chem to sell water filter business to Glenwood PE for $692 million

KT&G eyes overseas M&A after rejecting activist fund's offer

Kyobo Life poised to buy Japan’s SBI Group-owned savings bank

StockX in merger talks with Naver’s online reseller Kream

Meritz backs half of ex-manager’s $210 mn hedge fund

My memos got their start in October 1990, inspired by an interesting juxtaposition between two events. One was a dinner in Minneapolis with David VanBenschoten, who was the head of the General Mills pension fund. Dave told me that, in his 14 years in the job, the fund’s equity return had never ranked above the 27th percentile of the pension fund universe or below the 47th percentile. And where did those solidly second-quartile annual returns place the fund for the 14 years overall? Fourth percentile! I was wowed. It turns out that most investors aiming for top-decile performance eventually shoot themselves in the foot, but Dave never did.

Around the same time, a prominent value investing firm reported terrible results, causing its president to issue an easy rationalization: “If you want to be in the top 5% of money managers, you have to be willing to be in the bottom 5%, too.” My reaction was immediate: “My clients don’t care whether I’m in the top 5% in any single year, and they (and I) have absolutely no interest in me ever being in the bottom 5%.”

These two events had a strong influence on me and helped define my – and what five years later became Oaktree’s – investment philosophy, which emphasizes risk control and consistency above all. Here’s how I put it 33 years ago in that first memo, titled The Route to Performance:

I feel strongly that attempting to achieve a superior long-term record by stringing together a run of top-decile years is unlikely to succeed. Rather, striving to do a little better than average every year – and through discipline to have highly superior relative results in bad times – is:

-

- less likely to produce extreme volatility,

- less likely to produce huge losses which can’t be recouped and, most importantly,

- more likely to work (given the fact that all of us are only human).

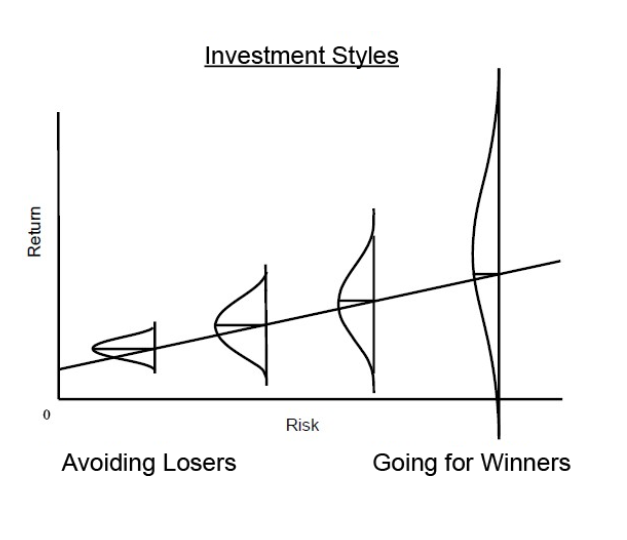

Simply put, what [General Mills’s] record tells me is that, in equities, if you can avoid losers (and losing years), the winners will take care of themselves. I believe most strongly that this holds true in my group’s opportunistic niches as well – that the best foundation for above-average long-term performance is an absence of disasters.

As you can see, my dinner with Dave was a seminal event; his approach was clearly the one for me. (Incidentally, I want to share that after decades of not having been in touch, Dave was among the many kind people who wrote in recent months to encourage me vis-à-vis my health issue. This is a great example of the many personal dividends my career has paid.)

Putting It in Brief

That first memo, and the bit cited above, include a phrase you’ve likely heard from Oaktree: If we avoid the losers, the winners will take care of themselves. My partners and I considered this phrase so fitting that we adopted it as our motto when Oaktree was formed in 1995. Our reasoning was simple: If we invest in a diversified portfolio of bonds and are able to avoid the ones that default, some of the non-defaulters we buy will benefit from positive events, such as upgrades and takeovers. That is, the winners will materialize without our having explicitly sought them out.

We thought that phrase was innovative. But in 2005, while working with Seth Klarman to update the 1940 edition of Benjamin Graham and David Dodd’s Security Analysis – the “bible of value investing” – I read something that indicated we were late by about 50 years. In the section Seth asked me to edit, I came across Graham and Dodd’s description of “fixed-value” (or fixed-income) investing as “a negative art.” What did they mean?

At first, I found their observation cynical, but then I realized what they were saying. Let’s assume there are one hundred 8% bonds outstanding. Let’s further assume that ninety will pay interest and principal as promised and ten will default. Since they’re all 8% bonds, all the ones that pay will deliver the same 8% return – it doesn’t matter which ones you bought. The only thing that matters is whether you bought any of the ten that defaulted. In other words, bond investors improve their performance not through what they buy, but through what they exclude – not by finding winners, but by avoiding losers. There it is: a negative art.

One more anecdote concerning the origin of the phrase: I’ve always been interested in old books. A few years ago, while walking through a Las Vegas convention center on the way to meet with a client, I came upon a rare book fair. I stopped at the booth of a book dealer I know, and my eye immediately fell on a book he had for sale: How to Trade in Stocks, by Jesse Livermore. Here’s the quote the dealer had highlighted: “Winners take care of themselves; losers never do.” You may be tempted to believe Livermore borrowed my idea . . . until you realize that, like Graham and Dodd, he published these lines in 1940. So much for my innovation.

At the time I adopted that saying, my partners and I were primarily high yield bond investors. And since non-convertible bonds have little upside potential beyond their promised yield to maturity, it truly was the case that our main job was to avoid the non-payers, with the assumption that some subset of the payers would likely give us exposure to positive developments that occurred. It was an appropriate way to sum up our approach as bond investors.

But fortunately, I joined up with Bruce Karsh in 1987, and in 1988 we organized our first distressed debt fund. Now we were investing in bonds that had defaulted or seemed likely to do so. We thought we might be able to buy them at bargain prices because of the cloud they were under, giving us the possibility of capital appreciation. Bruce has since become well known for his investing acumen, and, certainly, his returns since 1988 can’t be attributed to the mere avoidance of losses. When you aspire to returns well above those available on bonds, it’s not enough to avoid losers; you actually have to find (or create) winners from time to time. The returns generated by Bruce and his group show that they’ve done so.

Oaktree now has a number of what I call “aspirational strategies,” meaning they need winners. So why do we still use the above phrase as our motto, and why is “the primacy of risk control” still the first tenet of our investment philosophy? The answer is we want the concept of risk control to always be top of mind for our investment professionals. When they review a security, we want them to ask not only “How much money can I make if things go well?” but also “What will happen if events don’t go as planned? How much could I lose if things get bad? And how bad would things have to get?”

Risk control is still number one at Oaktree. Seventy-plus years ago, UCLA football coach Henry Russell “Red” Sanders said, “Winning isn’t everything, it’s the only thing.” (The saying is also attributed to Vince Lombardi, legendary football coach of the Green Bay Packers.) While I haven’t figured out exactly what that phrase means, I’m firmly convinced that for Oaktree, risk control isn’t everything; it is the only thing.

Not Risk Avoidance

Understanding the distinction between risk control and risk avoidance is truly essential for investors. Risk avoidance basically consists of not doing anything where the outcome is uncertain and could be negative. And yet, at its heart, investing consists of bearing uncertainty in the pursuit of attractive returns. For this reason, risk avoidance usually equates to return avoidance. You can avoid risk by buying Treasury bills or putting your money into government-insured deposits, but there’s a reason why the returns on these are generally the lowest available in the investment world. Why should you be well paid for parting with your money for a while if you’re sure to get it back?

Risk control, on the other hand, consists of declining to take risks that (a) exceed the quantum of risk you want to live with and/or (b) you wouldn’t be well rewarded for bearing. I’ve written in the past about what I call “the intelligent bearing of risk for profit.” Here’s the backstory:

I got my start managing money in 1978, when Citi asked me to run portfolios of convertibles and high yield bonds. The former were mostly non-investment grade securities issued by companies that had no alternative when seeking to raise capital, and the latter were, according to the terminology of the day, low-rated “junk bonds.” Clearly, they both entailed significant credit risk. Around 1980, a reporter from one of the first financial news networks asked me a provocative question: “How can you buy high yield bonds when you know some of the issuers are going to default?” My response captured the essence of intelligent risk bearing: “How can life insurance companies insure people’s lives when they know they’re all going to die?”

The point is simple: These functions can both be performed in an intelligent, risk-controlled way. For that to be the case, the risk has to be:

- risk you’re aware of,

- risk you can analyze,

- risk you can diversify, and

- risk you’re well paid to assume.

Risks like this needn’t be avoided. If you have real insight, such risks can be borne prudently and profitably.

I know several investors who take much more risk than Oaktree does and whose bad years are much worse than ours. But the few who possess genuine skill – what I call “alpha” (more on that later) – produce jumbo returns in their good years, such that their long-term returns are exceptional. Their clients are well rewarded . . . assuming they have enough intestinal fortitude to hang in through the bad years. Thus, risk-taking isn’t unwise per se, and risk avoidance is appropriate only for investors who feel they can’t survive tough times.

Building a Good Record

Since (a) all but the most cautious investing entails risk and (b) the presence of risk means results will be unpredictable and inconsistent, very few (if any) investors are able to have only good years or to assemble portfolios that contain only winners. The question isn’t whether you’re going to have losers, but rather how many and how bad relative to your winners.

Warren Buffett – arguably the investor with the best long-term record (and certainly the longest long-term record) – is widely described as having had only twelve great winners in his career. His partner Charlie Munger told me the vast majority of his own wealth came not from twelve winners, but only four. I believe the ingredients of Warren’s and Charlie’s great performance are simple: (a) a lot of investments in which they did decently, (b) a relatively small number of big winners that they invested in heavily and held for decades, and (c) relatively few big losers. No one should expect to have – or expect their money managers to have – all big winners and no losers.

In fact, not having any losers isn’t a useful goal. The only sure way to achieve that is by not taking any risk. But, as I said earlier, risk avoidance is likely to result in return avoidance. There’s such a thing as the risk of taking too little risk. Most people understand this intellectually, but human nature makes it hard for many to accept the idea that the willingness to live with some losses is an essential ingredient in investment success.

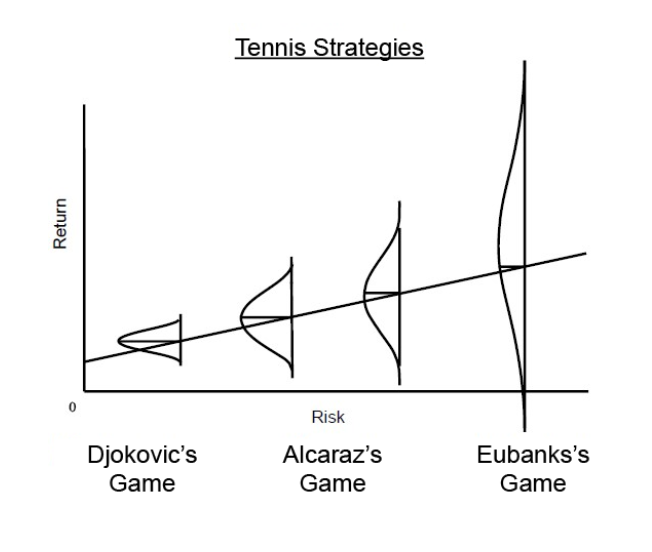

Having watched some great tennis this summer – right through the U.S. Open this past weekend – I’ll recycle a tennis analogy I first suggested in my memo Dare to Be Great II (April 2014). What if I went out to play tennis and said, “Today, I’m not going to commit any service faults”? My serves would have to be so meek that my opponent would likely destroy them. Tennis players have to take some risk if they hope to succeed (see below). If none of your serves fall outside the service box, you’re probably serving too cautiously to win. The same is true of investing. As my long-time partner Sheldon Stone puts it, “If you don’t experience any defaults, you’re probably not taking enough credit risk.”

Winners’ Stats

Looking back, it turns out I devoted an entire memo to analogies between investing and sports once per decade in the 1990s, the 2000s, and the 2010s. This time, in my fourth decade of memo-writing, I’m going to devote a few more paragraphs to tennis.

As mentioned above, tennis makes for very apt comparisons to investing. Hit safely and get blasted? Or try for shots you can’t make consistently and beat yourself? Charles D. Ellis’s article “The Loser’s Game” (The Financial Analysts Journal, July/August 1975) was truly seminal in my development as an investor. He pointed out that there are two kinds of tennis players . . . actually, two different types of tennis games. Professionals play a winner’s game: They win by hitting winners (in tennis, that means shots the opponent can’t return). Since their game is so much within their control, they can usually produce the shots they want, the best of which win points. But amateur tennis is a loser’s game: The winner is usually the person who hits the fewest losers. If you can just keep the ball in play long enough, eventually your opponent will hit it off the court or into the net. The amateur doesn’t have to hit winners to win, and that’s a good thing, because he or she generally is incapable of doing so dependably.

A quick look at some statistics from this year’s Wimbledon provides a great deal of food for thought. I’ll look first at the men’s quarterfinal match between Daniil Medvedev, the #3 seed in the tournament, and unseeded Christopher Eubanks. Eubanks, 6’7” and highly athletic, surprised everyone with his rush to the quarterfinals. But, in Medvedev, he was playing someone who’s spent years trailing just behind the “big three” of men’s tennis: Novak Djokovic, Rafael Nadal, and Roger Federer.

As a pronounced underdog, Eubanks probably recognized that he wasn’t likely to outlast or out-steady Medvedev. Thus, he had to go for winners. If that was Eubanks’s plan, he succeeded in executing it. He achieved 74 winners to Medvedev’s 52, and he aggressively rushed the net 67 times (for 44 winners) compared to Medvedev’s 8 (for 4 winners). These are great offensive stats.

The problem is that – as I’ve experienced firsthand many times – if you’re up against a player who’s better than you are, you have to attempt shots that aren’t firmly within your competence in order to have a hope of winning. Thus, along with his 74 winners, Eubanks was guilty of 55 unforced errors (mistakes that aren’t forced by good shots from one’s opponent; the easy way to make an unforced error is to go for a winner and miss). In comparison, Medvedev committed only 13 unforced errors.

Bottom line: Eubanks had considerably more winners than Medvedev, but he had three unforced errors for every four winners, whereas Medvedev had only one per four. Medvedev won 53% of the points played versus Eubanks’s 47%, and thus he won the match. The lesson is that it’s not enough to have more winners. To win – in tennis as in investing – you have to have a favorable relationship between winners and losers. You can win by having a few winners but fewer losers or by having a lot of losers but more winners. Neither maximizing winners nor minimizing losers is necessarily enough. It’s all in the balance.

And that leads me to the Wimbledon men’s final. This exciting match pitted Djokovic, who had won the most Grand Slam championships in history (23 combined at Wimbledon, the U.S. Open, the French Open, and the Australian Open), against up-and-coming 20-year-old Carlos Alcaraz, who had a grand total of one. Like Eubanks, Alcaraz plays a big, athletic game and goes for a lot of winners. You can see that in his serving: Alcaraz had seven double faults, more than twice Djokovic’s three. But, again, a single statistic tells us very little, since Alcaraz’s attempts at big serves gave him nine aces (serves his opponent couldn’t even get his racquet on), more than four times Djokovic’s two. This is an indication of the players’ respective styles. In the end, Alcaraz won the match with 66 winners, whereas Djokovic had only 32.

So, Alcaraz beat Djokovic with a “bigger,” high-risk game, while Medvedev beat Eubanks with his steadier, risk-controlled style. Neither approach is better than the other per se. Style alone never determines outcome; it’s a matter of style plus execution. My tennis teacher, Jordi Ballester, explains: “Alcaraz plays a more aggressive game. Given his high level of talent, as he showed at Wimbledon, if he has a good day, he can beat Djokovic (or any other opponent). If he’s off, he may well lose.”

It’s interesting to note that tennis’s big three presided over an incredible era. In the 19 years leading up to Wimbledon 2023, they won a combined 65 – or 87% – of the 75 Grand Slam championships. Notably, none of them was a “big hitter” in Alcaraz’s mold. Their ability to hit at a fabulous level for four or five hours without committing many errors was usually enough.

The Need for Winning Stocks

There have been several times over the course of my career when a small number of stocks have accounted for a disproportionately large share of the market’s gains. In this regard, a lot has been written about the so-called “magnificent seven”: Apple, Microsoft, Alphabet (owner of Google), Amazon, Nvidia, Tesla, and Meta (owner of Facebook). At various points in time this year, these seven stocks accounted for most or all of the gains of various equity indices. Here’s how the Financial Times put it in June:

Seven of the biggest constituents . . . have ripped higher, gaining between 40 per cent and 180 per cent this year. The remaining 493 companies [in the Standard & Poor’s 500 stock index] are, in aggregate, flat.

Big tech companies dominate the index to an unprecedented degree. Just five of those seven stocks represent nearly a quarter of the market capitalisation of the entire index. (“The seven companies driving the US stock market rally,” Financial Times, June 14, 2023.)

The extent of these stocks’ outperformance for much of this year may be unique, but the phenomenon is not. It was also the case in 2017 that a few stocks were largely responsible for carrying the market upward. Then it was the “FAANGs”: Facebook, Amazon, Apple, Netflix, and Google/Alphabet. The Financial Times highlighted this history as well:

Top-heaviness, particularly in US markets, is not new. “The big tech stocks in the S&P now are the same situation as oil companies were in the past, or the Nifty 50 in the 1960s,” says Frédéric Leroux, head of the cross-asset team at Carmignac in Paris – a nod to the craze that swept shares in a small number of fast-growing companies such as IBM, Kodak and Xerox higher before a heavy decline set in. “It’s a problem, but it’s a recurring problem.” (Ibid.)

For as long as most of us can remember, active investors have had a tough time keeping up with the equity indices. For this reason, in recent decades, passive investing has taken a substantial share of equity capital invested. Active investing’s shortfall has been attributed primarily to the combination of market efficiency, management fees, and investor error. I think there’s another reason: active investors’ need for winners.

What if you didn’t own the magnificent seven earlier this year? Clearly, you’d be far behind the indices. What if you owned them, but in smaller proportions than their weightings in the indices? You’d still lag, but by a smaller amount. So, by definition, keeping up with the indices requires having exposure to the big winners that is at least equal to their representation in the indices. That much seems clear.

Now, think about that representation. Let’s say you started off 20 years ago – in the summer of 2003 – with an index-sized helping of Apple at a split-adjusted price of $0.37. The key question is simple: Would you have held on as it rose?

As I described in my memo Selling Out (January 2022), most investors subscribe to the conventional wisdom of “taking profits,” “taking some money off the table,” or “topping the trees.” After all, as the old saying goes, “No one ever went broke taking profits.” Investors often sell off some of their winners for the simple reason that they’re afraid to watch as they give up their gains, which can lead to regret, criticism from clients, and/or lost accounts.

Most people would have sold part or all of their Apple holding by the time the price reached $15 in the summer of 2013. What would you have done when it hit 40 times your original cost after 10 years?

Today, another 10 years later, Apple is around $1801 – up 12x since 2013 and up by almost 500x since 2003. The point is, in the face of these gains, very few investors would still hold all they’d originally bought. But if they sold Apple stock when the constructors of the index didn’t, they’ve probably failed to keep up with the index. The situation can be summed up as follows:

- The performance of the equity indices is often dominated by a few stocks or groups of stocks.

- The gains of the leaders can make them seem expensive, arguing for profit-taking.

- Human nature – especially the desire to avoid regret – adds to the motivation to sell.

- By definition, if you reduce your holdings of the winners relative to their representation in the indices and these winners continue to outperform, you’ll have a tough time keeping up.

In my memo Liquidity (March 2015), I included an insight from my son Andrew. To paraphrase, he said, “If you look at the chart of a stock that’s been up for 25 years and say, ‘Man, I wish I’d owned that stock,’ think about all the days you would have had to talk yourself out of selling.” I doubt many people watched Apple go from $0.37 to $180 without selling any. How many active investors would allow Apple shares to constitute nearly 8% of their portfolios, which was its weight in the S&P 500 at the recent peak? But – to oversimplify – if they sold Apple, they’ve lagged.

The bottom line is that winners aren’t entirely dispensable. If you hope to at least keep up with the indices, you probably have to have an average representation in them. (This isn’t entirely inescapable. You might also achieve that goal by holding fewer of the losers.)

The Role of Risk Bearing

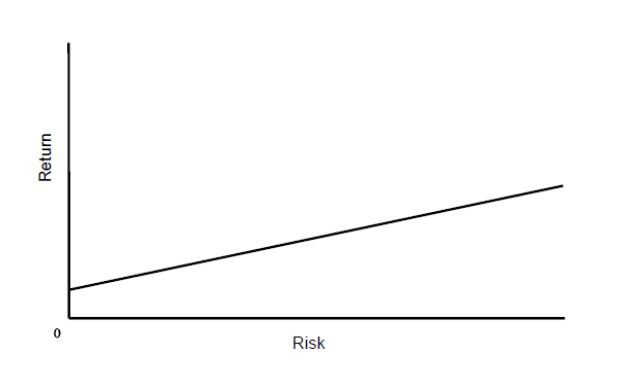

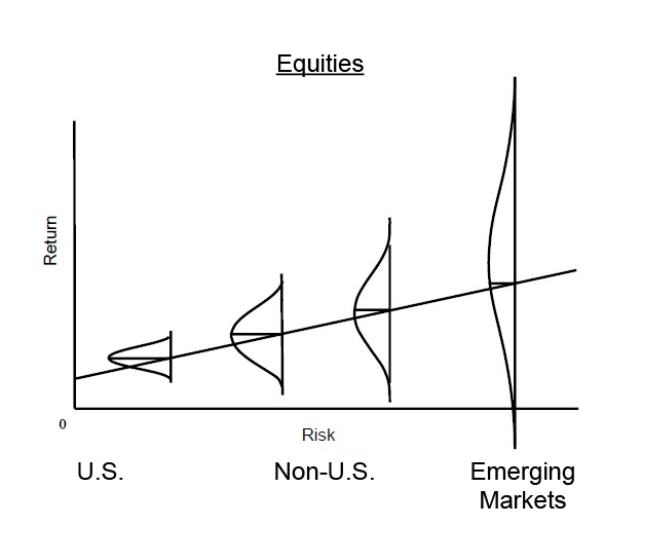

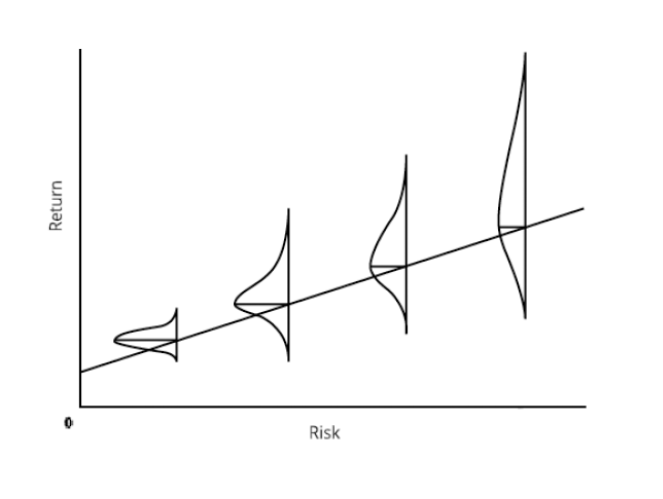

I’m going to conclude this memo using my favorite graph. When I attended graduate school at the University of Chicago 55 (!) years ago, I was taught to view the relationship between risk and return as follows:

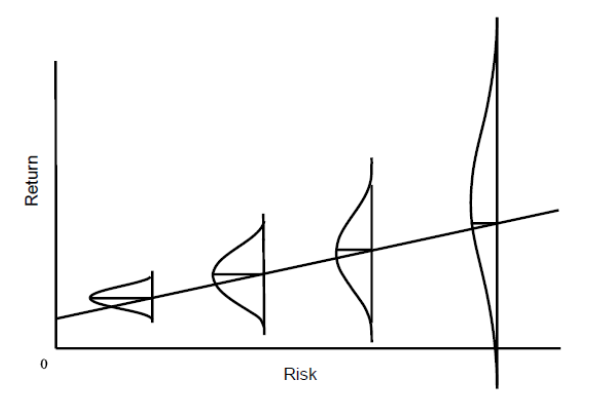

But the more I thought about it, the more unhappy I was with the way the linear presentation of the purported relationship tells investors that they can count on achieving higher returns as a result of taking more risk. After all, if that were really the case, risky investments wouldn’t be riskier. Thus, in my memo Risk (January 2006), I suggested a different way of depicting the relationship by superimposing on the line a series of bell-shaped probability distributions turned on their side:

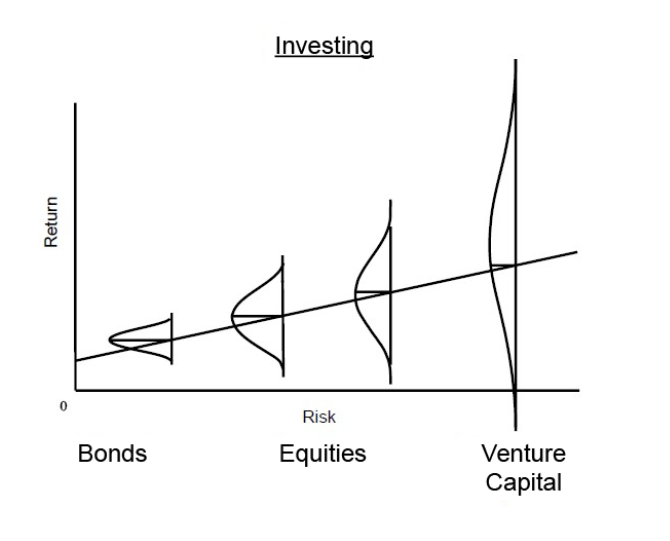

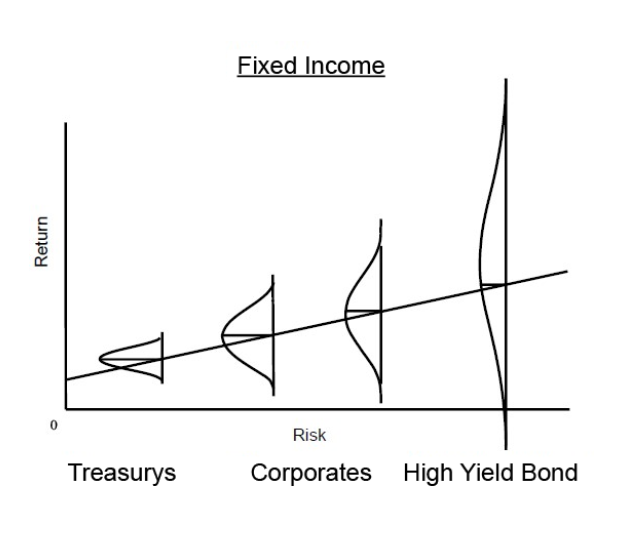

Rather than implying that taking more risk – moving from left to right in the graph – assures higher returns, this new way of looking at the relationship suggests that as you take more risk, (a) the expected return increases, as per the original version above; (b) the range of possible outcomes becomes wider; and (c) the bad possibilities become worse. In other words, riskier investments introduce the potential for higher returns, but also the possibility of other less-desirable side effects. That’s why they’re described as being riskier. Since writing that memo, I’ve concluded that this way of thinking about things has a great many applications. Here are a few:

There are also applications for this way of seeing things outside the investment world. For example:

And that brings me back to the subject of this memo:

As the above graphs indicate, a high-risk approach introduces the potential for huge returns . . . as well as the possibility of loss.

So, where’s the right place to be on this spectrum? Where can one find the best risk/return bargains? The short answer is that, according to investment theory – particularly the Efficient Market Hypothesis – there are no better (or worse) places to be. The EMH says markets price securities such that (a) their price equals their intrinsic value and (b) bearing incremental risk is rewarded fairly. Thus, bargains and over-pricings can’t exist. This is why, according to the theory, “you can’t beat the market.”

The theory also suggests that if a market is at “equilibrium,” each change in prospective return is fair relative to the change in risk borne, such that all positions on the curve are equivalent in attractiveness. Move to the left, and you avoid some risk, but your prospective return drops. Move to the right, and your prospective return increases, but so does your risk. No position on the spectrum is superior to any other. It’s like a coin toss (which the EMH suggests active investing is): Neither heads nor tails is the smarter call.

What About in Practice?

One of my favorite quotes is attributed to Albert Einstein and Yogi Berra, among others: “In theory, there is no difference between theory and practice. In practice, there is.” If markets are efficient and securities are always priced correctly, there can be no value in active investing. The truth is that many active managers, especially in developed market equities, have failed to demonstrate the ability to add value, or to add enough value to justify their management fees. This is largely why index funds were created and why a significant amount of equity capital has migrated to index and passive investing in recent decades.

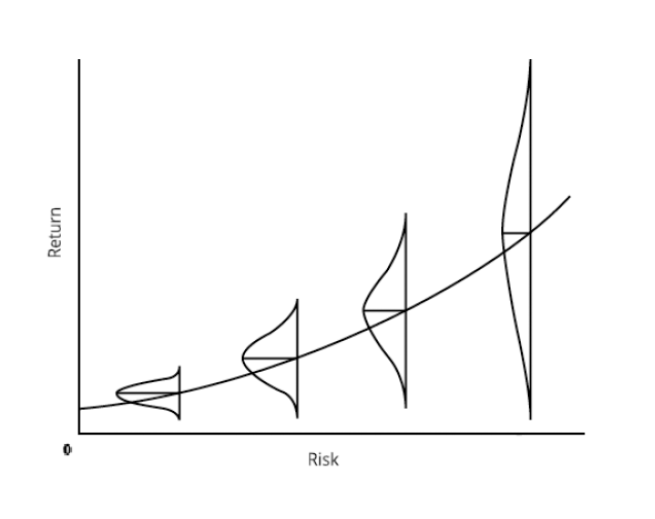

And yet, I firmly believe there are times when the markets are overpriced and times when they’re underpriced. There are also times when particular markets or sectors are overpriced or underpriced relative to others. In these instances, some securities can be priced too high or too low, and thus some positions on the risk curve can offer better bargains than others.

The theory assumes investors are rational and objective, but psychological excesses violate that assumption. Take, for example, the investment environment during the Global Financial Crisis. As I described in my July memo Taking the Temperature, in late 2008, investors were so worried about a financial sector meltdown that they panicked and sold securities aggressively as their prices collapsed. Excessive risk aversion causes the risk/return line to steepen (increasing the return for each incremental unit of risk borne) and perhaps even to curve upward (rendering the compensation for making investments at the risky end of the spectrum disproportionately generous). Thus, in periods of excessive risk aversion, the riskier part of the curve can be the smarter place to be (and in periods when risk bearing is too eagerly embraced, the safer part can offer a superior proposition).

The last element I want to touch on is what I call “alpha,” or individual investing skill. The reason the EMH disdains efforts to beat the market is its conviction that since securities are always priced correctly, the ability to identify bargains to buy and over-pricings to avoid can’t exist. Theory’s assertion that there’s no such thing as mastery of markets implies that no one has the skill to assemble portfolios that outperform. This is why I depict the bell-shaped curves above as symmetrical: In an efficient market, investors can only take what the market gives them.

But I’m convinced the potential to improve on that through skill does exist in some markets and some people. Investors who possess alpha have the ability to alter the shape of the distributions in the graphs above so that they’re not symmetrical, in that the portion of the distribution representing the less desirable outcomes is smaller than the portion representing the better ones. In fact, that’s what alpha really means: Investors with alpha can go into a market and, by applying their skill, access the upside potential offered in that market without taking on all the downside risk. In my memo What Really Matters? (November 2022), I said the key characteristic of superior investing is asymmetry – having more upside than downside. Alpha enables exceptional investors to modify the probability distributions such that they are biased toward the positive, resulting in superior risk-adjusted returns.

If alpha is the ability to earn return without taking fully commensurate risk, investors possessing it can do so by either reducing risk while giving up less return or by increasing potential return with a less-than-commensurate increase in risk. In other words, skill can enable some investors to outperform by emphasizing aggressiveness and some by emphasizing defensiveness. The choice between these approaches depends on the type of alpha an investor possesses: Is it the ability to produce stunning returns with tolerable risk, or the ability to produce good returns with minimal risk? Almost no investors possess both forms of alpha, and most possess neither. Investors who lack alpha shouldn’t expect to be able to produce either version of asymmetry – that is, to be able to generate superior risk-adjusted returns. However, most believe they do have it.

The proper choice between the two approaches – fewer losers or more winners – depends on each investor’s skill, return aspiration, and risk tolerance. As with many of the things I discuss, there’s no right answer here. Just a choice.

September 12, 2023

ENDNOTES

1This reflects the price as of September 8, 2023.

LEGAL INFORMATION AND DISCLOSURES

This memorandum expresses the views of the author as of the date indicated and such views are subject to change without notice. Oaktree has no duty or obligation to update the information contained herein. Further, Oaktree makes no representation, and it should not be assumed, that past investment performance is an indication of future results. Moreover, wherever there is the potential for profit there is also the possibility of loss.

This memorandum is being made available for educational purposes only and should not be used for any other purpose. The information contained herein does not constitute and should not be construed as an offering of advisory services or an offer to sell or solicitation to buy any securities or related financial instruments in any jurisdiction. Certain information contained herein concerning economic trends and performance is based on or derived from information provided by independent third-party sources. Oaktree Capital Management, L.P. (“Oaktree”) believes that the sources from which such information has been obtained are reliable; however, it cannot guarantee the accuracy of such information and has not independently verified the accuracy or completeness of such information or the assumptions on which such information is based.

This memorandum, including the information contained herein, may not be copied, reproduced, republished, or posted in whole or in part, in any form without the prior written consent of Oaktree.

More to Read

-

-

The KED ViewDon’t dwell on Korea discount; light up visibility on global stage

The KED ViewDon’t dwell on Korea discount; light up visibility on global stageJul 10, 2024 (Gmt+09:00)

-

-

-

Comment 0

LOG IN